A week or two ago on Twitter, CEO of NSW dairy body Dairy Connect Mike Logan made an intriguing reference to a “blueprint for NSW dairy”. There’s only a limited amount you can learn from the 140 characters of a tweet, so I invited Mike to elaborate on Milk Maid Marian and here’s what he had to say:

Mike Logan, Dairy Connect CEO

In the NSW dairy industry the issue is that the value chain is not adding value at the farm gate. Since deregulation the farmers have descended from being strategic partners in the value chain, to an input that must be minimised.

Perhaps this is similar around the rest of Australia – I am not qualified to say. However, it is easy to assume that the dairy model in NSW is flawed as we watch our cousins across the ditch (dutch) grow their businesses, convert sheepmeat farms to dairy and build new kitchens. (The ‘New Kitchen Meter’ is a reasonable measure of success in agriculture.)

It is also easy for the NSW dairy industry to look at the New Zealand dairy industry and suggest we should emulate their model of ‘one big co-operative’. Without doubt that is the best model in the world at the moment. I call it the United Soviet Socialist Republic of Dairy (USSRD) and Barnaby Joyce says that Fonterra is a Maori word meaning ‘single desk’.

As much as we would like to, we shouldn’t emulate their model.

Firstly, because we can’t. The legislation required would make the current budget look easy. Between Clive Palmer and David Leyonhjelm it would be a nightmare.

Secondly, it is because we need to think about the next model after New Zealand. What is better than the USSRD?

Our current model of the value chain in NSW dairy seems to look a bit like this:

Sort of messy eh?

The real problem with that value chain is that the farmer is held a long way from the representative of the consumer – otherwise known as the retailer. There are lots of ticket clippers, gatekeepers and a few value adders in the chain. There is not sufficient transparency and doubtful equity. The last person to make any money is the farmer.

So who is making the money?

Well, certainly the retailer. Here in Australia we have two of the three most profitable supermarkets in the world (Woolworths then Walmart then Coles/Wesfarmers).

Also the banks. The four most profitable banks in the Western world are right here. I needn’t name them. There are more profitable banks in China and Russia.

The distribution and transport sector is quite profitable. Linfox is not going out backwards.

Oddly, the processing sector in dairy is not making that much money. They are making more than the farm sector, but not an inordinate amount more. They only have about 25% of the capital invested when compared to the farm sector but they are mostly in control of the milk, its destiny and its value. They are the gatekeepers. The profit of the processors precedes the profit of the farmers.

So, what would a better model look like in NSW?

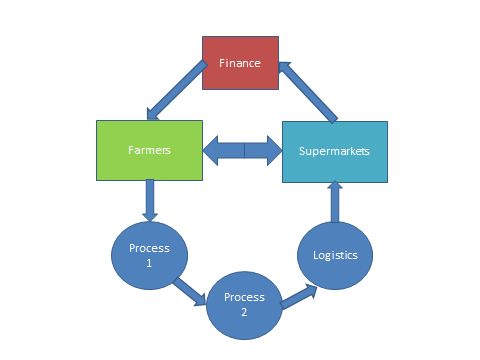

We suggest a value chain that is circular. We could call it a ‘value cycle’;

The most important part of the value cycle is that the farmers and the retailers are side by side. The needs and values of the farmers and the supermarkets align. They align because the farmers have a secure supply of a high quality product and the supermarkets need a secure supply of a high quality product. Both want transparency and equity.

The first time I saw the value cycle work in NSW dairy was with the Woolworths Farmers’ Own brand and the group of seven dairy farmers in the Manning. The farmers were told by their processor that they couldn’t get any more money from the supermarkets for their fresh milk. They were told how tough it is dealing with the supermarkets. To their credit, the farmers took the challenge and decided to find out how tough it is to deal with the supermarkets.

The processor was half right. It is tough to deal with the supermarkets, but there was more money available. Both the supermarket and the farmers got what they needed because their values aligned. The system is transparent and equitable.

If that is right here in Australia, is it right in the export market?

Yes it is. Along with Norco and the logistics company Peloris Global Sourcing, the NSW dairy industry facilitated by Dairy Connect has developed contacts in the retail sector in China for the sale of fresh milk. Again, the milk is worth more with a direct deal with the consumers. The model does work.

It is easy to scoff at the volumes for fresh milk to China, I will tell you that they are small but they are invaluable.

If we can deliver albeit small volumes of fresh milk into the fastest growing dairy consumer market in the world at a profit by developing direct relationships with the supermarket sector in China, then what is next?

Can we develop those relationships to deliver other NSW dairy products without having to enter the export commodity circus that is mostly controlled by the USSRD?

Of course we can. The NSW dairy industry is actively seeking investment and partnerships with the Chinese retail sector to access the infant formula market. Again, the processors are right, it is tough. The farmers in the Manning too are right; it will bring value back to the farm gate.