Don’t worry if you fall, just get back up again.

Wayne said the other day that the farm has taught him something about resilience: live in the moment when the sun is shining and, when the hail stings your skin, think of the big picture.

But the big picture right now is confusing for this Milk Maid. The WCB war has thrust the outlook for Australian dairy into the headlines and, with it, a lot of questions.

Our co-op has offered half a billion dollars for WCB, claiming that its loss to a global player would be “a tragedy”. In its statement to the ASX, MG Co-op said:

“The combination of MG and WCB is the only option available that delivers an Australian-owned and operated company with the scale, capacity, strength and momentum to service global growth opportunities, returning profits to dairy farmers and their communities.”

In the midst of all this, the UDV hosted a farmer forum on Monday where independent dairy analyst, Dr Jon Hauser, told farmers that supporting cooperatives is a “no brainer” but has also said the golden era of dairy in Asia was “largely rhetoric” and that real progress for Australian dairy would come through cost control and increased efficiencies at the farm and the factory.

He created a stir at the forum too, simply by saying that milk prices of 48 to 50 cents per litre could not be sustained. Not popular news.

So, now that Saputo is on the cusp of announcing a new offer, prompting WCB to ask for a suspension of trade, what if Helou’s tragedy does unfold? How will the General regroup?

MG will certainly have to work harder to woo those who harbour a co-operative spirit but supply other processors. And that, I’m afraid, is something the co-op has not done well to date, in my view. Perhaps the tide is beginning to turn, reading between the lines of Helou’s interview with The Weekly Times dairy writer, Simone Smith, headlined Divided we fall:

“There is nothing stopping our farmers rallying around a well-run farmer run company that is of scale and relevance.”

“There is no law in the land against that. That’s what we are advocating. This rally around the MG foundation to create a new farmer-owned business that is really relevant to the 21st century.

“The farmers will only benefit from direct ownership and direct influence in supply chain from the farm all the way to market.”

I guess we farmers are used to falling and getting back up again.

UPDATE: In response to a question asked below, Dr Hauser has kindly sent me this. I don’t know how to put it – complete with charts – in the comments section, so here it is instead:

Sorry Marian, It would take me a day to properly represent my position on the Asian growth story and even more to update my analysis to the most recent trade data.

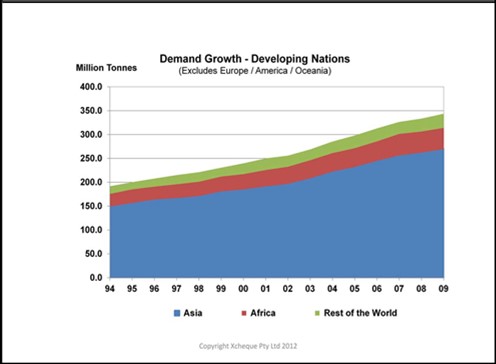

Here is a snapshot of the important data:

This is the demand growth for the developing nations. This comes from the FAO

Most of this growth has been serviced by internal development of their dairy industries.

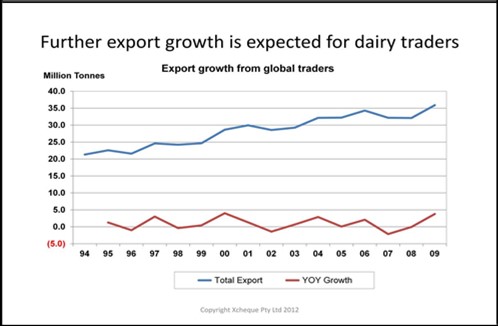

This the export growth from the key dairy traders – Europe, US, NZ, Argentina, Australia. The average is 2 – 3 billion litres / year. Even if this has been accelerating in the past few years it is unlikely that the opportunity is more than 4 – 5 billion litres / year. I believe the average growth opportunity for the global traders is 3 – 4 billion litres but I would need to review the more recent data to check this.

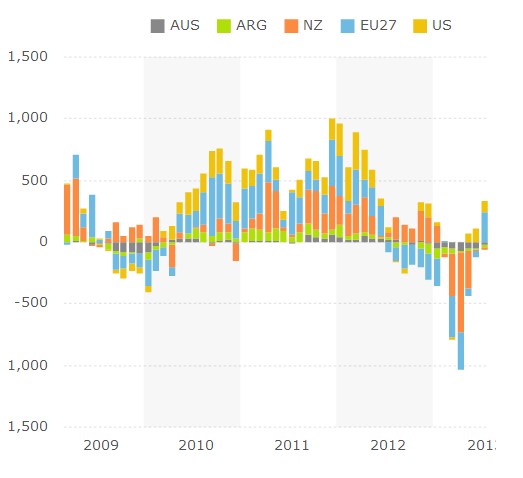

YOY Production milk production growth – Million Litres

This is the year on year growth that has come from the major traders. This chart shows 15 billion litres of growth from the EU, US, NZ and Argentina from July 2010 – June 2012. The total for the period from July 2009 – June 2012 is 12 billion. In other words we saw contraction in 2009 and 2012 and that is because the milk price was low. The US and Europe turn growth on or off according to commodity and milk price (New Zealand just keeps on trucking except when it doesn’t rain).

In summary:

- The Asia growth story is not rhetoric but the suggestion that the hole can’t or won’t be filled is.

- The US and Europe will turn on and off milk production according to demand and price. They had no difficulty growing supply at 5 billion litres / year in 2010 / 2011 and they are already gearing up to do it again in 2014.

- No I don’t subscribe to the analysis that has been done for the Horizon 2020 report. I believe the “Supply Gap” analysis is a flawed way of assessing Australia’s future export opportunity.

Hi Marian,

While the points you have raised from Monday night’s meeting in Warrnambool are correct, there is a significant risk that the context and real weight of meaning behind the points is missed.

Firstly,

48 to 50 c/l at the farm gate is not sustainable. This is because, as our domestic and export prices converge, these prices suggest a premium to the international market – therefore they are unsustainable. Why? Because product will come from somewhere else where it can be made and delivered more cheaply. We know how Australian consumers love stuff being delivered more cheaply from somewhere else – lots of proof there. Further, our relationship marketing on the global stage has its limits – they want our products – to a point.

If we want a premium to the export market, that is fine, we may be able to get a small one on the domestic market. The only problem with that, is that we need 6 billion litres less milk. A large number of the 43,000 directly employed people and many of the 100,000 additional industry support crew would need to find something else to do. Not to mention the vast number of communities which exist because of the dairy industry.

The reason people don’t like this is because the international market is volatile and has a ceiling. The only way to get more out of the system is for farmers and factories to become more efficient. Nobody likes this, but the reality is we don’t have a culture of either “celebrating success” or asking ourselves “how can I do this better tomorrow?”.

This is all heading to the point: increased farm and factory productivity is the key to sustainable growth of the Australian dairy industry. NZ has demonstrated how this can be done. In that case, a strong Coop is at the core. They have also demonstrated that it is hard and farmers need to be committed to the cause long term. For some reason, NZ has a far more positive and constructive attitude than we do. This leads to the second point.

Secondly.

Attitude is everything. People line up (albeit a minority) to vociferously denigrate the industry which has fed, clothed and educated their families for generations. Yet they still milk cows. They still want people to work on their farms. They look to others to solve their problems with debt or other cost of production decisions.

Attitude is everything. NZ has more farm debt than we do, operates in the same markets we do and have doubled production in the same time it has taken us to drop 2 billion litres. Go figure.

The UDV is attempting to convince the industry at large that this attitude and action must change if we are to have a Profitable, Australian Owned, Large Scale, Competitive Export Industry.

The bastards (the factories) aren’t ripping us off, they are working on our behalf. The 3 remaining “players”, Bega, MG and WCB were all founded on cooperative principles with the purpose of returning the best prices to farmers. It is up to us to ensure we retain ownership so we have a say in our own future.

Tyran Jones

UDV Vice President

LikeLike

Hi Tyran,

I really appreciate you fleshing out a couple of these points.I agree wholeheartedly with almost everything you say.

Not sure that the differences between NZ and Aus are all about attitude though. The drought might have had a bit to do with us falling behind, too. And the Kiwis must think the way MG is being hamstrung by its own government is hilarious.

LikeLike

Marian

Indeed, between attitude and regulatory environment, we can account for a lot of things. Attitude is king – just look at N Vic. Those who had the resources buckled down and got on with it (restructure, modify system etc). Now conditions have turned around (they have water) the tap has been turned on again, new entrants, restarts etc. Those who have experienced the NZ attitude speak very very highly of it. Their government also supports dairy much more than ours does. I don’t know enough about it, but would suggest it is much more cohesive with more detractors outside than in. There are some lessons there.

There is a major difference between Australia and just about every major dairy exporting country, except NZ (still had a structural advantage) – the dominant players grew up in a highly regulated environment where the intra country players all sat around and decided what the price should be. The poignant example here is Canada where they don’t let foreign investors in due to a claim “it is not in the national interest”. Canada retains perhaps the world’s most regulated dairy industry. Some countries have policies of actively encouraging consolidation and scale so they can compete internationally.

Tyran Jones

UDV Vice President

LikeLike

You’re right. Last night’s announcement illustrates our government’s disinterest in our dairy sector beautifully.

LikeLike

I struggle with this one Marian.

If the cooperative model is so much better then why doesn’t it provide greater returns to growers who supply the cooperative? Why hasn’t done so in the past?

If it doesnt supply greater returns, why is it so special? Feelgood factor about Australians controlling the company that sells their product? A vague unease about foreign companies taking over?

And the comments from the MG boss…please! They are just jingoistic nonsense and PR spin. One day MG was a great company competing internationally, the next day it cant survive without WCB. (It’s almost like Kirin don’t exist!)

One thing that does worry me is that the higher the bidding war goes, the higher the liklihood of large scale rationalision (processing job losses), regardless of the owner.

LikeLike

Thanks for the questions, Ian. People often make the same point: if the co-op is so good, why doesn’t it offer the best price?

The point is that the co-op provides the benchmark. All the other companies know they have to better MG’s price to retain supply. One company, in fact, has a policy of the MG price plus 1.5 cents per litre.

LikeLike

Thanks Marian

It does sound a little like rationalisation to me that you need a benchmark. Price matching or agreeing to better a competitor’s price is commonplace in most industries that I know about, without the need for such a benchmark company.

I guess (from a long way away!) I’d be hoping that the new guys bidding get the company. More competition to keep everyone on their game. The alternative is concentration of ownership and further consolidation of market power. Sound familiar?

LikeLike

I wish you were right but, no, the benchmark is very, very real. When you get a chance, please do read the post by Dr Hauser that I linked to “no brainer” up there. It really tells a story.

Keep tuned for more!

LikeLike

Hi Ian,

It is not about feel good factor, it is about being competitive on the international market. We are a net dairy exporter and the domestic and export prices have largely converged. It doesn’t matter what we want to think, our farm gate prices are determined by the international market.

We currently have a fragmented processing sector with many small players. The problem with this is the ability to invest in new efficient technology and equipment is hampered, doubling up of management etc. We are currently at a disadvantage to other dairy exporters on the two fronts of scale and efficiency. The two are linked. Monday night in Warrnambool Jon Hauser showed us some graphs about cost of manufacture. Small plants cost more to produce a unit of dairy product than bigger ones. Scale does matter. Both Bega and MG are talking about synergies, so this is factor as well, but is for them to identify and realise.

Importantly, this is not about farm gate competition, it is about us being a profitable, growing player in the global market. If we are not, we continue to contract towards a domestic market. The current fragmentation has delivered proof we need to change.

If we don’t retain Australian ownership of what is left of our industry, we will lose the lot in rapid succession and will just watch them destroy what is left and we will have no say. Foreign owners are not accountable to us, They are in it to boost their bottom line, not ours. Foreign owners of Australian dairy assets have a track record of paying too much, Trying to push milk price down to recover costs, Pulling out, or just plain coasting, paying around MG price + not much to maintain status quo with no investment or advantage provided to our local industry. Examples Fonterra, Lion, Parmalat, Kraft, Nestle, the list is long, the record poor.

I’m not advocating a monopoly, I’m advocating a strong, profitable, rationalised Australian owned, globally competitive, export industry. Foreign ownership will not achieve that. Surely we want to maintain some sort of balance of Australian ownership in the mix? There are only 3 left. Bega, MG and WCB. There is about to be 1 less.

You are right, rationalisation is required – in every other context it is called “productivity gains” or “productivity bonuses or dividends” etc. We need scale and we need people who are answerable to us to be running our industry.

Jon Haused also pointed out that dairy farmers have the most skin in the game here. For every $100m invested across the dairy supply chain, farmers have about $90m tied up in farms, cows, plant and equipment; and factories have about $10m invested in plant. Who has the most to lose here? We do!!

Why would we hand over control of our destiny and our massive investment to a foreign company who is not accountable to us in any way.

With recent events, it could all be over next week, so we’d better all be hoping Bega can prevail. We will then have 2 Australian owned companies of scale and capability we can work with for the best possible outcome for the Australian dairy industry.

This is about the future of our industry as an Australian owned, profitable, competitive export sector.

Tyran Jones

UDV Vice President

LikeLike

Hi Marian. I’m interested in another summary point you have drawn from Jon Hauser’s talk, that “the golden era of dairy in Asia was largely rhetoric”. The usual story here is that global dairy demand is growing faster than supply, largely driven by Asian demand, and that the Australian industry has a chance to grab some of this new demand. For example the Horizon2020 report estimates a nominal “shortfall” of about 8 billion litres by 2021, after taking into account expected supply growth in producing countries. Did Jon disagree with these demand projections, or is it more that he doesn’t think they will be associated with higher prices?

LikeLike

I’ll see if Jon will respond to this himself but my understanding of his position is that other faster growing dairy nations (like Argentina) will be the ones to capitalise on the Asian market.

LikeLike

Hi Marian,

It is a range of factors, but I think his point is really that the US and EU can rapidly increase production to fill any gaps (and has in the past). The US produces in a month what we produce in a year, so a very small percentage increase in production can deliver a couple of billion litres for export.

They respond almost immediately to price signals, switching supply on and off overnight (hence the price drop we saw last year in response to the higher prices the year prior)

Recent Rabobank reports also suggested the US is gearing up to better support the export markets, so they will potentially be more responsive than ever to global market signals.

Tyran Jones

UDV Vice President

LikeLike

Yes, Tyran. Have you seen the update from Jon I put in the body of the post?

LikeLike

Call me stupid (and you probably will) but how are we going to continue to compete on the world markets when we have such high labour and energy costs? NZ produces SMP at almost half the price we do.

LikeLike

Hi DB. I wouldn’t call anyone trying to work their way through the complexities of dairy stupid! What would that make me? 😉

I don’t know the answer to your question, except to say that the way forward seems to be:

a) innovation on farm and

b) greater efficiencies at the factory level, which is the reasoning behind MG’s bid for WCB. It’s chasing increased scale in order to meet the efficiencies of much larger processors and to reach new markets.

LikeLike

G’day all, observations from a non dairy farmer.

I might be going a bit off topic, but can I suggest the reason for US and EU switching supply on/off is the levels of farm subsidies. They probably produce that milk anyway but just waste whats not saleable. Yet another obstacle oz industry faces in a “level” playing field that is all uphill.

LikeLike

Interesting observation, David. The EU and US have reduced their farm subsidies significantly, which is great. There are still some there and other indirect subsidies (like environmental custodianship payments) but subsidisation is less of a factor than it once was.

LikeLike